The financial condition of a company is determined in several ways. One of them is an analysis of the liquidity of the enterprise’s balance sheet. Before looking at the coefficients in detail, you should understand the basic concepts.

Definition

The term liquidus was borrowed from German language in the twentieth century. Translated, it means "fluid". Liquidity is the ability of assets to mobilize, transform from material and other values into cash. This term is closely related to the solvency of the enterprise, that is, the ability of the organization to fulfill these obligations on time and in full. In a narrow sense, this means that the company must have enough money to pay off creditors.

IN Russian legislation a different interpretation of this concept is provided. According to the Law of the Russian Federation “On Insolvency,” enterprises that have overdue accounts payable for more than 3 months in an amount exceeding 100 thousand rubles are considered insolvent.

An analysis of the liquidity and solvency of the organization must be carried out before accepting any important decision, and also for:

Financial situation forecasting;

Monitoring the fulfillment of obligations to counterparties;

Increasing trust from partners;

Assessment of the effectiveness of credit use.

An analysis of liquidity and solvency is carried out based on balance sheet data. The presence of additional statistical information will only improve the quality of the data obtained.

Western economists conduct liquidity analysis to find out whether a company can:

- quickly pay off all short-term obligations;

- repay current debts in general;

- pay off all other obligations.

In order to answer each of these questions, a corresponding indicator is calculated.

Risks

According to Art. 19 Federal Law "OBU", economic entities are obliged to monitor the facts of economic life. Therefore, enterprises disclose financial indicators in annual reports and also provide information about possible problems V economic activity. In most cases, liquidity risk arises if an organization is unable to timely and completely repay existing obligations in relation to suppliers, contractors, loans and borrowings, etc.

Liquidity can be contrasted with profitability. The “good” assets do not generate any income (current account) or its size is very small (demand deposits for a period of 1 to 30 days). Long-term investments promise big dividends, but you have to pay for them with funds diverted from turnover for a long time. Analysis of the liquidity of the enterprise shows Current state organizations.

Directions of research

Solvency is an external reflection of stability and financial stability. If the company is liquid, then it can pay all obligations on time. Since the liabilities contain loans with different maturities, one of the areas of analysis is to group balance sheet items according to the speed of their sale.

Liquidity analysis shows how many obligations a company can cover and over what period of time. When selling assets, there is a risk of difficulties with the sale. It is defined as the difference between the “present value” and the potential price of the property. Liquidity management is the activity of an organization to allocate capital, which will allow turning assets into money in a short period of time.

First step

Balance sheet liquidity is the level at which a firm's liabilities are covered by its assets. This indicator can also be measured by the value of its own working capital: the more there are, the better. The analysis of the liquidity of assets and liabilities begins with dividing them into groups, according to the algorithm presented in the table below.

If A 1, A 2, A 3 is greater than P1, P2, P 3 and A 4< П 4 , то баланс абсолютно ликвиден. Но такая ситуация встречается кране редко.

Enterprise liquidity analysis: ratios

To find out the level of solvency of an organization, it is necessary to calculate several indicators:

1. Current liquidity ratio (CTL) shows the situation as a whole. It displays how many of the organization's current assets are per ruble of liabilities. The company pays off debts using available funds. That is, current assets must exceed liabilities. The critical value of the indicator varies by industry and type of activity, but in theory it should not exceed 2. Formula:

Ktl = ObA\KO, where:

ObA - current assets excluding debt with a maturity of more than 12 months;

KO - short-term liabilities without taking into account future income and expense reserves.

The value of the indicator is determined by the volume of long-term sources of financing. To increase it, you need to increase capital and reasonably restrain the growth of inventories.

An analysis of the liquidity of an enterprise's balance sheet based on this ratio does not provide a complete picture. The calculation does not take into account the structure of the operating system, in which some assets may be more liquid than others. Sometimes situations arise when the value of the coefficient remains within the normal range, but the company is experiencing problems with cash. If a company does not have enough funds to maintain the achieved scale of production, then this situation is called overexpansion. It can arise if the company is rapidly growing in momentum or if it was not fully funded in the previous stages. The way out of the situation is to obtain a long-term loan.

2. An analysis of the organization’s liquidity for a narrower range of assets is carried out on the basis of the intermediate solvency ratio (ISR). When calculating it, production inventories are not taken into account. The logic is quite simple. The proceeds from the sale of inventory may be less than the amount spent on purchasing it. Very often, upon liquidation, an enterprise will receive only 40% of their accounting value from the sale of materials and raw materials. The critical value of the coefficient is 1. Formula:

Kpl = (OA - Inventories) \ Short-term liabilities, where OA is current assets.

But liquidity analysis involves not only calculating indicators, but also identifying the reasons for their changes. Therefore, it is necessary to determine the factors that caused the changes. If the growth of the indicator was caused by an increase in unjustified debt, then this indicates negative dynamics.

3. Absolute liquidity (Kal). This is the most stringent evaluation criterion. The ratio shows what part of the obligations can be repaid with cash. The recommended lower limit is 0.2. In practice, not all enterprises achieve these values. The thing is that each industry must have its own standard, and all data obtained must be supplemented by an analysis of the solvency of competitors in the market. Absolute liquidity is calculated using the formula:

Cal = line 260 \ page (690 - 640 - 650), where line XXX is balance line No. XXX.

Timely repayment of accounts receivable (RA) is the main factor in the growth of this ratio.

Other indicators

1. The value of own working capital (COS) = Working capital (FC) + Inventories + DZ + Advances + Money in bank accounts (DC) + Short-term investments = II section of Assets - II section of Liabilities.

2. OS maneuverability. The ratio shows how much working capital is accounted for by the most liquid assets (money on hand and in bank accounts). A decrease in the value of the indicator may indicate both the repayment of the loan and the tightening of the conditions for obtaining trade credit from suppliers and contractors. An increase in the coefficient indicates positive dynamics and an increase in the ability to meet obligations.

There is another approach to calculating this indicator. Some economists recommend calculating it by dividing the cost of inventories and long-term reserves by the value of SOS. The standard value of the indicator depends on the field of activity of the enterprise: in capital-intensive industries its level should be less than in material-intensive ones. Formula:

Maneuverability of OS = DS \ (Current assets - Current liabilities).

3. How much current assets per unit of assets.

4. The share of SOS in OA.

5. The share of inventories in current assets: a large proportion of materials and raw materials in the warehouse can arise as a result of overstocking, for example, before holding promotions. But it also indicates a decrease in demand for products. Formula:

D z = Inventories \ OA = line (210+220) / line (290-230-217).

6. SOS share in reserves - shows what part of the raw materials is provided at their expense. The standard value is 0.5. Formula:

Share = SOS\Inventories.

7. Inventory coverage ratio - shows how the materials were purchased. Its positive dynamics indicate “normal” sources of financing, and its negative dynamics indicate that the raw materials were purchased using earthly capital.

Liquidity analysis and assessment is most often carried out on the basis of three ratios: instantaneous, current and quick liquidity.

New approach

Recently, the debt/EBITDA ratio, which is calculated as the ratio of liabilities to profit before tax, has become widespread. The numerator may contain a figure for short-term, long-term, total or net (less debt) debt. Depending on the calculation results, the borrower can be classified as unfavorable (4 or more), risky (3-4), moderate (2-3) and conservative (up to 2).

The interest coverage ratio (TIE) is calculated as the ratio of net cash flow to interest payments on borrowed funds. The higher it is, the lower the risk of default.

To improve the efficiency of solvency management, you need to draw up a payment calendar (PDDS), which displays the ratio of cash balances and expected receipts with the amounts of expenses for the same period.

Identifying reasons for deviation

The reasons for financial insolvency can be divided into several groups. The first includes economic (decline in production, bankruptcy of debtors), political (imperfect legislation), level of development of scientific and technological progress and other external factors. To mitigate their impact, an enterprise can, for example, attract additional sources of financing by issuing shares or diversify production (disperse assets across different types of activities).

The second group of internal factors includes those that depend on successful collaboration all departments of the organization: the presence of a deficit of SOS, growth of receivables, incorrect determination of the selling price. Paying off accounts receivable will greatly improve the condition of the organization. Factoring transactions or concluding an assignment agreement will speed up the turnover of funds.

Another option is to improve payment discipline. For example, enter into a collection agreement with a bank, under which the buyer will automatically be charged fines for each day of delay. The credit institution presents the corresponding requirement to the recipient of the goods for payment. This will significantly speed up cash turnover. This solution has its drawbacks: firstly, such a step must be specified in advance in the contract with the counterparty, and not every client will agree to such conditions. Secondly, fees for banking services must be comparable to the benefits received.

How to increase solvency

1. Change the structure of receivables: enter into an assignment or collection agreement with the bank.

2. Increase profits. Each organization has its own individual method.

3. Change the capital structure. The predominance of borrowed funds in liabilities reduces the liquidity of the balance sheet.

4. Increase SOS and reduce the share of reserves.

5. The enterprise cannot influence such external economic factors as the decline in production in the country. However, replacing obsolete equipment with newer ones, for example, through a leasing agreement, will improve the situation.

From theory to practice

To understand everything, let’s try to consider in practice how liquidity analysis is carried out. An example is given below.

Indicators for 2013 |

|||||

The value of the absolute liquidity ratio is below normal. Although it increased several times during the year, it decreased again at the end. The drop may be caused by the use of free cash to purchase inventories or poor collection of receivables.

The quick liquidity ratio has been constantly decreasing over the year. Although its values are higher than standard, the dynamics are negative. But for now, the company can cover current obligations using its own working capital.

In general, the liquidity analysis showed that the company is beginning to serious problems. Even minor delays in payment terms for products can lead to a lack of funds. There are several ways to correct the situation:

Increase equity capital (SC);

Sell part of the assets;

Reduce excess inventories;

Carry out work to collect debt;

Take out a long-term loan;

Renew or rent out unused OS.

Financial analysis: bank liquidity

By issuing loans, a lending institution reduces the amount of money stored. At the same time, the risk of non-return of the deposit increases. To prevent such a situation, reserves are used. The bank can turn to the Central Bank for a temporary loan. The presence of excess money stimulates the credit institution to invest it, for example, in securities.

Bank liquidity is the ability of an organization to fulfill its obligations in a timely manner. It is based on constantly maintaining a balance between the insurance company and attracted and placed funds. To do this, the bank needs to create a balance sheet structure in which various assets will quickly turn into cash. Liquidity analysis is carried out in two directions. Within the horizontal framework, the specific gravity is determined separate groups assets and liabilities. These indicators are compared with the total volume of transactions. A vertical analysis of a bank's liquidity, which is carried out on the basis of a net balance, provides information about groups and types of transactions.

The level of solvency of a credit institution can also be calculated using ratios. They are divided into two groups:

Regulatory ones, which are established by the Central Bank and must be complied with by all banks;

Estimated ones, which are developed by specialized companies or analytical services. It is not necessary to achieve their values, but calculation will provide more complete information.

Summary

In order to control the level of development of an enterprise and timely identify risks of business activities, it is necessary to periodically carry out financial analysis in the following areas:

Solvency of the enterprise;

Level of business activity of the organization;

Cash flow control;

Building your own capital;

Financial stability of the organization, etc.

The analysis of liquidity indicators is carried out in several stages. First, assets and liabilities are divided into groups, and then solvency ratios (minimum three) are calculated. The results obtained must be compared over time across the enterprise and the industry as a whole.

The bank's solvency level must be monitored regularly. Its strong decline may force the credit institution to sell off part of its assets. As for the enterprise, the situation here is slightly different. Additional loans can increase your solvency, but you should not abuse them. It is better to focus your efforts on collecting debt, increasing equity capital, or selling unused assets.

In this article we will look at the current ratio, which shows the company’s ability to pay off current (short-term) obligations using only current assets.

Thanks to the simple calculation formula and information content, the current liquidity ratio has an important place in assessing the financial performance of various industries and is used in a number of effective techniques bankruptcy forecasting.

Current ratio. general information

Current (or total) liquidity ratio (k) is a financial value showing the ratio of current assets to current liabilities, or short-term liabilities, which is compiled on the basis of balance sheet information. It is also an indicator of the ability to repay short-term loans using working capital. The higher k is, the more solvent the company is. Its decrease indicates that assets are no longer urgently sold. General formula:

- k = (current assets) : (current liabilities).

Current assets:

- cash (including electronic money) at the cash desk, in bank accounts;

- accounts receivable + provision for bad debts;

- investments in securities;

- material assets and products for sale.

Current responsibility:

- loans for up to one year;

- unpaid obligations to suppliers and the treasury.

- other loans.

Deduction formula for assets and liabilities:

- k = (Al + Ab + Am) : (Ps + Pk), where

- Al – Liquid assets;

- Ab – quickly sold;

- Am – slowly being realized;

- Ps – Liabilities of fixed-term obligations;

- PC – short-term.

Balance formula:

- k = (p. 1200 + p. 1170) : (p. 1500 – p. 1530) – p. 1540).

Purpose of the total liquidity ratio

This value performs the following tasks:

- an indicator of the ability to pay off its obligations during the current production cycle;

- “litmus test” of the company’s solvency, its ability to cover all loans with available amounts;

- efficiency indicator of both a separate operating period and the chosen direction of product turnover;

- important information for investors;

- the components necessary for the formula for a given k are also used when calculating working capital.

Current ratio norm and deviations from it

Current ratio value:

| Short | Norm | High |

| < 1,5 | 1,5 -2,5 | > 2,5 |

| Difficulties in fulfilling obligations - the consequence should be the closure of accounts payable and a decrease in current assets, since the company will not be able to pay its obligations at this moment. However, such budget instability does not always lead to bankruptcy of the company | Illustrates how many rubles of current assets there are per ruble of current liabilities. Theoretically, such an enterprise will be able to meet its obligations in a timely manner at any time. | Current assets and goods are not used at the proper level - the availability of short-term loans should be expanded |

Important! When calculating, we must not forget that assets are unevenly liquid - it is necessary to take into account in detail the speed of their turnover (use the second formula).

Ways to increase the liquidity of an enterprise

To optimize k indicators, the following methods are used:

| Way | Actions | pros | Minuses |

| Increasing the profitability of core activities, keeping most of the income at your disposal | Dividend cut Reducing funding for non-productive purposes | Quickly bringing k into the normal range | Negative impact on the company’s image, trust of founders, shareholders |

| Reducing the number of projects whose source of financing is short-term capital | Reducing the amount of investments in construction, reconstruction, and purchase of expensive equipment | The company stops investing amounts exceeding its financial capabilities | Reflection on the level of compliance with international standards for equipment and conditions of production and other activities |

| Limitation of financing through short-term loans | Using short-term debt only to replenish working capital; a multi-year loan is used to cover other expenses | Investment of long-term programs is carried out using a long-term loan and current income | The emergence of new loan obligations |

| Changes in money management principles | Programs to improve the efficiency of working capital management | General modernization of business methods | Suitable only for companies whose increase in working capital is due to financing through short-term loans |

| Debt restructuring to creditors | Offsetting and subsequent write-off in the form of unclaimed amount | Getting rid of overwhelming debt | Complex, trust-breaking process |

Important! Shortk True liquidity is not an indicator of a company's cash shortage. Since current assets include receivables, investments, products, etc.

Calculation of the indicator using the example of AVTOVAZ

| Index | year 2014 | 2015 | 2016 |

| Working capital | 49 783 | 40 073 | 55 807 |

| Short-term loans | 86 888 | 112 867 | 117 723 |

Using the general formula:

- k (2014) = 49,783/ 86,888 = 0.00001151;

- k(2015) = 40,073/112,867 = 0.00000886;

- k (2016) = 55,807/117,723 = 0.4740535.

Average current liquidity indicator by industry of the Russian Federation

| 2013 | 2014 | 2015 | 2016 | 2017 | |

| Agriculture | 1,7644 | 1,7437 | 1,7678 | 1,7651 | 1,862 |

| Construction | 1,327 | 1,2474 | 1,2069 | 1,251 | 1,243 |

| Oil and gas industry | 1,8771 | 1,7718 | 1,8343 | 1,7849 | 2,3887 |

| Trade enterprises | 1,6426 | 1,6931 | 1,658 | 1,7146 | 1,6006 |

| Industry (metallurgy) | 1,5689 | 1,5572 | 1,5297 | 1,592 | 1,5261 |

| Small business (hotel, restaurant service) | 1,4887 | 1,1795 | 1,2726 | 1,5998 | 1,2305 |

| General indicators for the country | 1,7143 | 1,6764 | 1,5012 | 1,5389 | 1,4903 |

Comparison with other liquidity ratios

Comparative table of existing liquidity deduction ratios:

| kabsolute liquidity | ktotal liquidity (current) | kquick liquidity | |

| Essence | Analyzes liquidity by calculating k between the company's total budget, its equivalent and current loans | Possibility to repay short-term debt using working capital | The ability to repay a loan using your fastest cashable assets, for example, in case of sudden difficulties in selling the company's goods. Indicator of financial stability |

| Peculiarities | Credit profile of the company. Does not take into account debts of debtors, inventories of goods and unsold products - only monetary assets available in this moment. Evaluates the current ability to respond to your loans | General information about solvency, including its assessment for one production period. Data on the ability to cash out your products. Indicators for its calculation can be used in the formula that subtracts working capital | In some ways similar to deducting k total liquidity, but shifts the focus to a narrower area, excluding inventories - the slowest part of assets in terms of liquidity. In assessing solvency, the method is more conservative and cautious |

| Calculation formula | K= ((monetary assets) + (short-term investments)) : (short loans) | K = (current assets) : (current loans) | K = ((monetary assets) + (short-term investments) + (debts of debtors)) : (current short-term liabilities) |

| Normal values | <0,2 – неимение возможности ответить по обязательствам при помощи только оборотных средств; 0.2 – 0.5 – normal solvency; >0.5 – unclaimed monetary assets in banks, irrational investments | <1,5 – трудности в покрытии долгов; 1.5-2.5 – solvency is normal; >2.5 – irrational distribution of assets, infringement in the financing of any industries | 0.7-1 is the norm; loans taken and provided by the company are approximately equivalent. Below 0.7 – there is a possibility of a shortage of liquid quantities. More than 1: the company’s desire to provide loans to debtors in larger quantities than acquiring such obligations for itself |

| Application | Calculation is necessary for future suppliers who require payment using term loans | The indicators of this k are of greater interest to investors | Wide range: for managers – assessment of the company’s financial performance; for creditors – checking the financial stability of the enterprise and the risks associated with it; for investors - forecast of return on investment |

Important! The norms of the coefficients may vary depending on the industry of the enterprise.

Using the current ratio in predicting bankruptcy

The current liquidity ratio is one of the values that allows you to calculate the state of affairs of a company in the future - bankruptcy or prosperous activity. When making calculations, Edward Malton's formula is often used:

- B = – 0.3877 – 1.0736 x k l + 0.0579 x k n. (k l – current liquidity ratio, k n – concentration of hired funds):

- В > 0 – the probability of bankruptcy is low;

- B = 0 – 50/50;

- IN< 0 – чем выше величина, тем вероятнее разорение.

The advantage of the formula is its simplicity. However, it is not adapted for Russian business, since it was created using reporting as an example foreign countries, so there is a possibility of forecast error. A more accurate formula is the so-called four-phase, but with different components:

- B = (8.38 x A 1) + A 2 + (0.054 x A 3) + (0.63 x A 4), where

- A 1 – working capital/asset;

- A 2 – net income/own budget;

- A 3 – profit from the sale of products/asset;

- A 4 – net revenue/integral expenses.

Important! It is believed that this formula is capable of predicting the future of the company with a result of up to 80%.

What does a negative current ratio show?

In the literal sense, the value of the indicator cannot be a negative number - it can be small down to one ten-thousandth. Progressive negative dynamics of the value indicate the following:

- wrong financial policy company and distribution of funds;

- oversaturation of obligations to creditors;

- large volume of unsold products;

- about excessive investment;

- availability large quantity debts outstanding to the company.

- probable imminent bankruptcy.

Methods for assessing financial condition using the current liquidity indicator

Basic assessment methods involving the coefficient:

- Selezneva-Ionova model. The methodology is aimed at comparing actual indicators with the standard, identifying the profitability of assets in terms of their net income, as well as an overall assessment of the company's management.

- Saifullin-Kadykov model. Similar to the previous one, it may be true for analyzing the financial status of companies of various industries and sizes. The success of sales and turnover of your own budget is also calculated.

- Postyushkov's model. Suitable for assessing the prediction of the ruin of an enterprise with a prediction range of up to six months.

Current ratio: current issues

Answer: All information is taken from the company’s annual financial report and accounting documents.

Question No. 2: Should we focus on the all-Russian norms of the current liquidity ratio?

Answer: Only for information ownership. For each industry, depending on the subject of the Russian Federation where it operates, k indicators vary greatly.

Question No. 3: For whom should k total liquidity be calculated first?

Answer: This information is useful for the head of the enterprise to have, and it may also be required by your creditors and investors.

Question No. 4: If my calculated ratio is high - more than two, does that mean my business is moving in the right direction?

Using the absolute liquidity ratio, they determine what part of immediate debts can be repaid using cash and their analogues (securities, bank deposits and so on.). That is, through highly liquid assets.

The absolute liquidity ratio, along with other liquidity indicators, is of interest not only to the management of the organization, but also to external subjects of analysis. Thus, this ratio is important for investors, quick liquidity is important for banks; and absolute – to suppliers of raw materials and supplies.

Definition and Formula in Excel

Absolute liquidity shows the short-term solvency of the organization: whether the company is able to pay off its obligations (with counterparties-suppliers) using the most liquid assets (cash and cash equivalents). The coefficient is calculated as the ratio financial resources to current liabilities.

The standard calculation formula looks like this:

Cubs. = (cash + short-term cash investments) / current liabilities

Cubs. = highly liquid assets / (most urgent liabilities + medium-term liabilities)

The data for calculating the indicator is taken from the balance sheet. Let's look at an example in Excel.

We have circled the lines that are needed to calculate the absolute liquidity ratio. Balance formula:

Cubs. = (p. 1240 + p. 1250) / (p. 1520 + p. 1510).

Example calculation in Excel:

We simply substitute the values of the corresponding cells (in the form of links) into the formula.

Absolute liquidity ratio and standard value

Accepted in foreign practice normative meaning coefficient – > 0.2. The essence of the restriction: every day the company must repay at least 20% of current liabilities. Practice financial analysis V Russian companies adheres to the same principles. True, there is no justification for this approach.

Structure of short-term debt in Russian practice heterogeneous. Repayment terms fluctuate significantly. Therefore, the figure 0.2 should be considered insufficient. For many enterprises, the norm of the coefficient is in the range of 0.2-0.5.

If the absolute liquidity ratio is below normal:

- the enterprise cannot immediately pay off with suppliers using funds of all types (including proceeds from the sale of securities);

- Economists need to further analyze solvency.

A large increase in the absolute liquidity ratio shows:

- too much most of non-performing assets in the form of cash on hand and in bank accounts;

- needed additional analysis application of capital.

Thus, the higher the ratio, the higher the liquidity of the company. But excessively high values indicate irrational use of funds: the company has an impressive amount of finances that are not “invested in the business.”

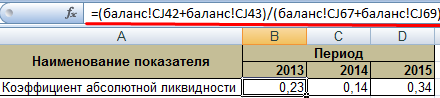

Let's return to our example.

The values of absolute liquidity in 2013 and 2015 are within normal limits. And in 2014, the company experienced difficulties in paying off short-term obligations.

Let us illustrate the dynamics of the indicator and for clear example display on the graph:

To produce full analysis solvency of the enterprise, calculate all indicators of the liquid current assets of the organization. This ratio is used to calculate the share of short-term liabilities that can realistically be repaid immediately. The example shows that the value for the period 2011-2015. increased by 0.24. In 2011, 2012 and 2014, the company experienced solvency difficulties. But the situation has returned to normal - the company is able to fulfill current obligations by 34%.

The ability of any enterprise to pay its bills can be assessed by analyzing accounting documents.

Liquidity is a term that characterizes the property of an enterprise's assets. Liquid assets can be quickly sold at market price and converted into cash. If it is a product, then this means the speed of its sale at a nominal price. Only money has absolute liquidity.

There is also the liquidity of an enterprise, which refers to its solvency to other entities. It determines how quickly a company is able to pay off debt using working capital.

Assets and liabilities

When conducting financial analysis, it is necessary to analyze the existing assets and liabilities of the enterprise.

Assets according to the degree of liquidity are divided:

- highly liquid– enterprise cash and securities (A1);

- liquid– accounts receivable for shipped goods, which will be returned within a short time (A2);

- low liquidity– long-term investments, inventories of goods, production that is not completed (A3);

- illiquid– non-current assets (A4).

The liabilities of the organization can also be divided into groups:

- urgent– debts to creditors (P1);

- moderately urgent– loans that must be repaid within one year (A2);

- non-urgent– loans and long-term loans (A3);

- permanent– capital and financial reserves (A4).

Liquidity ratios

The liquidity of an enterprise is calculated on the basis of certain instruments, which are liquidity ratios. The current ratio is used by investors, the quick ratio by creditors, and the absolute ratio by suppliers to clarify the company’s ability to pay its obligations.

The liquidity of an enterprise is calculated on the basis of certain instruments, which are liquidity ratios. The current ratio is used by investors, the quick ratio by creditors, and the absolute ratio by suppliers to clarify the company’s ability to pay its obligations.

A company's ability to pay off debt with current assets is called current liquidity. It is calculated like this:

- K=A1+A2+A3/P1+P2

A coefficient value less than one means complete insolvency.

Quick ratio similar to the previous indicator, but inventories are not taken into account here. Formula for calculation:

- K=A1+A2/P1+P2

He says that if it is impossible to quickly sell goods, how quickly will the company pay off its obligations.

If cash and short-term investments are classified as short-term liabilities, then it turns out absolute liquidity ratio. The formula for calculating it is:

- K=A1/Π1+Π2

The main difference between these indicators is that current and quick liquidity ratios characterize the solvency of the organization in the medium and long term, and the absolute indicator - in the short term.

It is necessary to strive for the norm of the absolute liquidity ratio not less than 0.2, which means the possibility of daily payment of 20% to creditors. This is part of the short-term liabilities that will be repaid in the near future using available cash.

The indicator is considered by analysts to be one of the most stringent criteria for a company's liquidity. As a rule, companies are experiencing a shortage of cash, so it is often lower than normal.

There are situations when the coefficient value reaches 0.5, which is higher than normal. This may indicate that the company suddenly has a lot of free cash in its accounts, which for some reason is not used in the production process. Therefore, an overestimated value does not indicate a very good solvency of the company.

There are situations when the coefficient value reaches 0.5, which is higher than normal. This may indicate that the company suddenly has a lot of free cash in its accounts, which for some reason is not used in the production process. Therefore, an overestimated value does not indicate a very good solvency of the company.

When analyzing the indicator, you need to know exactly how the specifics of the industry influence the level of solvency. Here, much depends on the speed of turnover of current assets and liabilities.

The ratio increases when liabilities to other enterprises in the short term, inventories and non-current assets decrease and long-term financing of the enterprise increases. But this does not always affect solvency.

It is worth considering the volumes of sales and production of products, on which current liabilities directly depend. If volumes are stable or constantly growing, then debt obligations will in any case be repaid and new ones created, because this process is continuous.

Therefore, it is better to use these coefficients either at the initial stage of the enterprise’s existence or during its liquidation.

For more information about what can be learned based on this indicator, watch the following video:

Balance calculation

In the balance sheet, assets and liabilities are assigned codes. If you have a completed one for a certain period, you can easily calculate the coefficient using indicators with the following codes:

- K=(1240 + 1250)/(1520 + 1510 + 1550)

So, code 1240 includes investments within one year. These include securities and debt obligations of other enterprises. Code 1250 – money, including at the cash desk, in current accounts, transfers. 1510 are loans, 1520 are accounts payable, code 1550 in the balance sheet includes other liabilities.

One of the indicators of a company's performance is the level of liquidity. It assesses the creditworthiness of the organization, its ability to fully pay off its obligations on time. More details about what liquidity ratios exist and formulas for the new balance sheet for calculating each indicator are presented in the article below.

The essence

Liquidity is the extent to which liabilities are covered by the firm's assets. The latter are divided into groups depending on the period of transformation into cash. This indicator evaluates:

- the firm's ability to respond quickly to financial problems;

- ability to increase assets with increasing sales volumes;

- opportunity to repay debts.

Liquidity levels

Insufficient liquidity is expressed in the inability to pay debts and assumed obligations. We have to sell fixed assets, and in the worst case, liquidate the organization. The deterioration of the financial situation is expressed in a decrease in profitability, loss of capital investments of owners, delay in payment of interest and part of the principal debt on the loan.

The quick liquidity ratio (the balance sheet formula for calculation will be presented below) reflects the ability of a business entity to repay debt using the available funds in its accounts. Current solvency may affect relationships with customers and suppliers. If an enterprise is unable to repay its debt on time, its continued existence is in doubt.

Any liquidity ratio (the balance sheet formula for calculation will be presented below) is determined by the ratio of the organization’s assets and liabilities. These indicators are divided into four groups. In the same way, any liquidity ratio (the balance sheet formula for calculation is needed to analyze activities) can be determined separately for quickly and slowly sold assets and liabilities.

Assets

Liquidity is the ability of an enterprise's assets to generate a certain income. The speed of this process is precisely reflected by the liquidity ratio. The balance formula for calculations will be presented below. The larger it is, the better the enterprise “stands on its feet.”

Let's rank assets according to the speed at which they are converted into cash:

- money in accounts and cash registers;

- bills, treasury securities;

- non-overdue debts to suppliers, loans issued, Central Bank of other enterprises;

- stocks;

- equipment;

- structures;

Now let's distribute assets into groups:

- A1 (the most liquid): funds in cash and in a bank account, shares of other enterprises.

- A2 (quickly sold): short-term debt of counterparties.

- A3 (slowly realized): inventories, work in progress, long-term financial investments.

- A4 (difficult to sell) - non-current assets.

A specific asset belongs to one or another group depending on the degree of use. For example, for a machine-building plant lathe will be classified as “inventory”, and the unit manufactured specifically for the exhibition will be classified as a non-current asset with a useful life of several years.

Liabilities

The liquidity ratio, the formula for the balance sheet of which is presented below, is determined by the ratio of assets to liabilities. The latter are also divided into groups:

- P1 – the most popular obligations.

- P2 - loans with a validity period of up to 12 months.

- P3 – other long-term loans.

- P4 - enterprise reserves

The lines of each of the listed groups must coincide with the degree of liquidity of assets. Therefore, before making calculations, it is advisable to modernize the financial statements.

Balance sheet liquidity

To carry out further calculations, it is necessary to compare the monetary values of the groups. In this case, the following relationships must be met:

- A1 > P1.

- A2 > P2.

- A3 > P3.

- A4< П4.

If the first three of the listed conditions are met, then the fourth will be fulfilled automatically. However, a shortage of funds in one group of assets cannot be compensated by an overabundance in another, since quickly sold funds cannot replace slowly sold assets.

In order to carry out a comprehensive assessment, the total liquidity ratio is calculated. Balance formula:

L1 = (A1 + (1/2) * A 2 + (1/3) * A3) / (P1 + (1/2) * P2 + (1/3) * P3).

The optimal value is 1 or more.

The information presented in this way is not replete with details. A more detailed calculation of solvency is carried out based on a group of indicators.

Current liquidity

The ability of a business entity to repay short-term obligations using all assets is shown by the current liquidity ratio. Balance formula (line numbers):

Ktl = (1200 – 1230 – 1220) / (1500 – 1550 – 1530).

There is also another algorithm by which you can calculate the current ratio. Balance formula:

K = (OA - long-term debt - debt of the founders) / (short-term obligations) = (A1 + A2 + A3) / (Π1 + Π2).

The higher the indicator value, the better the solvency. Its standard values are calculated for each industry, but on average they range from 1.49 to 2.49. A value less than 0.99 indicates the enterprise’s inability to pay on time, and a value greater than 3 indicates a high proportion of unused assets.

The coefficient reflects the solvency of the organization not only at the current moment, but also in emergency circumstances. However, it does not always provide the complete picture. U trading enterprises the value of the indicator is less than the normative one, and for production ones it is most often higher.

Urgent liquidity

The ability of a business entity to repay obligations using quickly salable assets minus inventory reflects the quick liquidity ratio. Balance formula (line numbers):

Ksl = (1230 + 1240 + 1250) / (1500 – 1550 – 1530).

K= (term. DZ + multiple. financial investments + DS) / (term. loans) = (A1 + A2) / (Π1 + Π2).

In the calculation of this coefficient, like the previous one, reserves are not taken into account. From an economic point of view, the sale of this group of assets will bring the most losses to the enterprise.

The optimal value is 1.5, the minimum is 0.8. This indicator reflects the share of liabilities that can be covered by cash flows from current activities. To increase the value of this indicator, it is necessary to increase the volume of own funds and attract long-term loans.

As in the previous case, an indicator value greater than 3 indicates an irrationally organized capital structure, which is caused by slow inventory turnover and an increase in accounts receivable.

Absolute liquidity

The ability of a business entity to repay debt with cash reflects. Balance formula (line numbers):

Cal = (240 + 250) / (500 – 550 – 530).

The optimal value is more than 0.2, the minimum is 0.1. It shows that the organization can pay off 20% of its current liabilities immediately. Despite the purely theoretical probability of the need arising urgent repayment of all loans, you must be able to calculate and analyze the absolute liquidity ratio. Balance formula:

K= (short-term financial investments + DS) / (short-term loans) = A1 / (Π1 + Π2).

The calculations also use the critical liquidity ratio. Balance formula:

Kcl = (A1 + A2) / (P1 + P2).

Other indicators

Maneuverability of capital: A3 / (JSC - A4) - (P1 + P2).

Its decrease in dynamics is considered a positive factor, since part of the funds frozen in inventories and accounts receivable is released.

Share of assets in the balance sheet: (balance sheet total - A4) / balance sheet total.

Provision of own funds: (P4 - A4) / (JSC - A4).

The organization must have at least 10% of its own sources of financing in the capital structure.

Net working capital

This indicator reflects the difference between current assets and loans and accounts payable. This is that part of the capital that is formed through long-term loans and own funds. The formula for calculation is:

Net capital = OA - short-term loans = line 1200 - line 1500

The excess of working capital over liabilities indicates that the company is able to pay off debts and has reserves for expanding its activities. The standard value is greater than zero. A lack of working capital indicates the organization’s inability to pay off obligations, and a significant excess indicates an irrational use of funds.

Example

The company's balance sheet includes:

- Cash (DC) – 60,000 rubles.

- Short-term investments (SFI) – 27,000 rubles.

- Accounts receivable (RA) – 120,000 rubles.

- OS - 265 thousand rubles.

- Intangible assets - 34 thousand rubles.

- Inventories (PZ) – 158,000 rubles.

- Long-term loans (LC) – 105,000 rubles.

- Short-term loan (CC) – 94,000 rubles.

- Long-term loans – 180 thousand rubles.

Cal = (60 + 27) / (105 + 94) = 0.4372.

The optimal value is more than 0.2. The company is able to pay 43% of its obligations using funds in its bank account.

Let's calculate the quick liquidity ratio. Balance formula:

Ksl = (50 + 27 + 120) / (105 + 94) = 1.09.

The minimum value of the indicator is 0.80. If the company uses all available funds, including accounts receivable, then this amount will be 1.09 times more than existing liabilities.

Let's calculate the critical liquidity ratio. Balance formula:

Kcl = (50 + 27 + 120 + 158) / (105 + 94) = 1.628.

Interpretation of results

The coefficients themselves do not carry any meaning, but in terms of time intervals they characterize in detail the activities of the enterprise. Especially if they are supplemented with other calculation indicators and a more detailed consideration of assets that are taken into account in a specific balance sheet line.

Unliquid inventories cannot be quickly sold or used in production. They should not be taken into account when calculating current liquidity.

In an organization that is part of a holding group, when calculating the liquidity ratio, indicators of internal receivables and payables are not taken into account. The level of solvency is best determined by the absolute liquidity ratio.

Overvaluation of assets will cause many problems. Inclusion of unlikely debt collection in calculations leads to an incorrect (reduced) assessment of solvency and the receipt of unreliable data on the financial position of the organization.

On the other hand, if assets are excluded from the calculations, the probability of receiving income from which is low, it is difficult to achieve standard values of liquidity indicators.

43. Liquidity ratios: current, urgent and absolute.

Liquidity– the ability of assets to be quickly sold at a price close to the market. Liquidity is the ability to convert into money.

Current liquidity

Current (total) liquidity ratio (coverage ratio; English current ratio, CR) - financial ratio, equal to ratio current (current) assets to short-term liabilities (current liabilities).

Ktl = (OA - DZd) / KO, where: Ktl – current ratio; OA – current assets; DZd – long-term receivables; KO – short-term liabilities.

The ratio reflects the company's ability to pay off current (short-term) obligations using only current assets. The higher the indicator, the better the solvency of the enterprise.

A coefficient value of 2 or more is considered normal (this value is most often used in Russian regulations; in world practice, 1.5 to 2.5 is considered normal, depending on the industry). A value below 1 indicates high financial risk due to the fact that the company is not able to consistently pay current bills. A value greater than 3 may indicate an irrational capital structure.

Quick (urgent) liquidity

- financial ratio equal to the ratio of highly liquid current assets to short-term liabilities (current liabilities). The source of data is the company’s balance sheet in the same way as for current liquidity, but inventories are not taken into account as assets, since if they are forced to be sold, losses will be maximum among all current assets.

Kbl = (Short-term accounts receivable + Short-term financial investments + Cash) / Current liabilities

The ratio reflects the company's ability to pay off its current obligations in the event of difficulties with the sale of products.

A coefficient value of at least 1 is considered normal.

Absolute liquidity

Absolute liquidity ratio- financial ratio equal to the ratio of cash and short-term financial investments to short-term liabilities (current liabilities). The source of data is the company’s balance sheet in the same way as for current liquidity, but only cash and funds close to it in essence are taken into account as assets:

Cal = (Cash + short-term financial investments) / Current liabilities

Unlike the two above, this coefficient is not widely used in the West. According to Russian regulations, a coefficient value of at least 0.2 is considered normal.

44. Forecasting solvency indicators.

When deciding on attracting credit resources, it is necessary to determine the creditworthiness of the enterprise.

On modern stage The following coefficients are accepted:

Current liquidity ratio (coverage), K p;

Coefficient of provision with own working capital, K os;

Coefficient of restoration (loss) of solvency, K uv.

These indicators are calculated based on balance sheet data using the following formulas:

The coefficient K p characterizes the overall provision of the enterprise with working capital for conducting business activities and timely repayment of the enterprise's urgent obligations.

The coefficient K uv shows whether the enterprise has a real opportunity to restore or lose its solvency within certain period. The basis for recognizing the balance sheet structure as unsatisfactory and the enterprise as insolvent is the fulfillment of one of the following conditions: K p< 2 или К ос >0.1. It should be remembered that when deciding whether to issue a loan from a bank or other credit organization, the following system of financial ratios is calculated:

Absolute liquidity ratio K al;

Intermediate coverage coefficient K pr;

Overall coverage coefficient K p;

Independence coefficient Kn.

The absolute liquidity ratio shows the proportion of short-term liabilities that can be repaid using highly liquid assets and is calculated using the formula, the standard value of the indicator is 0.2 – 0.25:

The intermediate coverage ratio shows whether the company will be able to pay off its short-term debt obligations on time. It is calculated by the formula:

Calculating the total coverage ratio is similar to determining the current ratio. The financial independence ratio characterizes the enterprise's provision of its own funds to carry out its activities. It is determined by the ratio of equity to the balance sheet currency and is calculated as a percentage.

The optimal value that ensures a fairly stable financial position in the eyes of investors and creditors: 50 – 60%.

45. Own and borrowed resources of the enterprise

Borrowed and own funds of the enterprise - collectively determine the liquidity of its assets, and directly affect the size of financial and other funds that provide the opportunity to use them at a specific moment or period of time.

Borrowed funds allow an enterprise to increase production, turnover, gain additional profit and even pay off previous debts and much more.

In addition to borrowed funds, to obtain certain financial advantages, an enterprise can also use attracted funds, which, unlike borrowed funds, are not actually repaid - for example, equity shares and gratuitous government financing.

Ordinary entrepreneurs can also actively use borrowed funds. Public policy Russian Federation for Development entrepreneurial activity, by raising borrowed funds from various sources, provides for obtaining interest-free loans in accordance with current legislation. In addition, such loans are not taxed.

Taxes will only be on the income received, in the case of a cash loan - in the case of a material loan, the material benefit is not calculated. You can use borrowed funds constantly or regularly if it is effective and has a stable profit, or is a necessity.

However, it is advisable to monitor very carefully and pay attention to debt-to-equity ratio and maintain a clearly defined balance - it is good to have a certain strategy of action in case of unforeseen circumstances, since in the case of using borrowed funds, there is a certain threshold of financial losses, beyond which you will not be able to restore your business and will immediately or after a certain time become bankrupt.

Here, it is also necessary to take into account - gearing ratio- it can be approximately calculated by dividing the total amount of existing loans and interest charges on them by total assets and future income.

The value of this coefficient will be one of the fundamental factors in granting you loans, that is, the lower the coefficient, the greater the likelihood of receiving a loan.

In general, it is advisable to use gratuitous and especially reimbursable borrowed funds only when you are already well on your feet and understand your business segment.

Now, the state legislation of the Russian Federation provides for free subsidies for opening a private business, in the form of partial financing of initial capital - but it does not provide guarantees of the success of its development.

Absolute liquidity ratio (Cash ratio)

Definition

Absolute (cash) liquidity ratio(cash ratio) shows the ratio of the organization's most liquid assets - cash and short-term financial investments - to short-term liabilities.

The absolute liquidity ratio is a variation of two other more common liquidity ratios: the current ratio and the quick ratio. Moreover, in calculating this indicator, only the fastest-selling (liquid) assets are used.

Calculation (formula)

The coefficient is calculated as follows:

Absolute liquidity ratio = (Cash + Short-term financial investments) / Current liabilities

All components of the formula are taken from the organization’s balance sheet.

Normal value

The absolute liquidity ratio is not as popular as the current and quick ratios and does not have a firmly established norm. Most often, a value of 0.2 or more is used as a guideline for the normal value of the indicator. However, too high a ratio indicates unreasonably high amounts of free cash that could be used for business development.

Read about the cash liquidity ratio in English in the article " Cash Ratio".

Current ratio

Definition

Current (total) liquidity ratio(current ratio) is a measure of the organization’s solvency, the ability to repay the organization’s current (up to a year) obligations. Lenders widely use this ratio in assessing the current financial position of an organization and the danger of issuing short-term loans to it. In Western practice, the ratio is also known as the working capital ratio.

Calculation (formula)

The current liquidity ratio is calculated as the ratio of current assets to short-term liabilities:

Current ratio = Current assets / Current liabilities

The numerator of the formula is taken from the assets of the balance sheet, the denominator - from the liabilities.

Normal value

The higher the current ratio, the higher the liquidity of the company's assets. A coefficient value of 2 or more is considered normal. However, in world practice it is allowed to reduce this indicator for some industries to 1.5.

A low value of the ratio (below 1) indicates probable difficulties in the organization's repayment of its current obligations. However, to complete the picture, you need to look at the cash flow from the operating activities of the organization - often a low ratio is justified by a strong cash flow (for example, in fast food chains, retail trade).

A current ratio that is too high is also not desirable, since it may not reflect enough efficient use current assets or short-term financing. In any case, lenders prefer to see a higher ratio as a sign of a company's sound position.

Read about the current ratio in English in the article " Cash Ratio".

Quick ratio

Definition

Quick ratio(quick ratio, acid-test ratio) characterizes the organization’s ability to pay off its short-term obligations through the sale of liquid assets. At the same time, liquid assets in in this case includes both cash and short-term financial investments, as well as short-term receivables (according to another version - all current assets, except for their least liquid part - inventories). The quick liquidity ratio has become widespread in Russian and world practice along with the current liquidity ratio.

Calculation (formula)

The quick ratio is calculated by dividing liquid assets by short-term liabilities:

Quick ratio = (Cash + Short-term financial investments + Short-term receivables) / Current liabilities

According to another version:

Quick ratio = (Current assets - Inventories) / Current liabilities

Inventories are considered the least liquid assets, they are considered the most difficult to convert into money (i.e., sell), so they are not included in the calculation in any case.

Normal value

The higher the quick ratio, the better the financial position of the company. A value of 1.0 or higher is considered normal. At the same time, the meaning may differ for different industries. If the ratio is less than 1, liquid assets do not cover short-term liabilities, which means there is a risk of loss of solvency, which is a negative signal for investors.

Absolute liquidity ratio

BALANCE

13.04.09

1. enlarging the interval;

2. folding the moving average;

3. analytical alignment.

The interval enlargement method is used to identify the trend of time series, where the main development trend is distorted by random deviations. The essence of the method: the transition from the initial series of dynamics to series of longer periods. For example, from months to quarters. As the intervals become larger, the overall trend becomes more noticeable.

As a result of enlarging the interval, the general trend in the development of trade turnover becomes obvious:

1. trade turnover increases from year to year;

2. the turnover of the second half of the year annually exceeds the turnover of the first half of the year;

3. The turnover of the fourth quarter is the largest;

4. the turnover of the first half of the subsequent year is always less than the turnover of the second half of the previous year;

5. The turnover of the same-named half-years increases from year to year.

Moving Average Smoothing. The essence of the method is that the initial values of this series are used to determine the calculated (theoretical values), in which random deviations are partially canceled out and the main development trend is revealed more clearly in the form of a smooth line. For the calculation, it is necessary to determine the links of the moving average. The number of levels in each link should be a year in duration, that is, for a quarterly series - a four-level link, for a monthly series - a twelve-level link. The calculation consists of determining the average value for each link. In this case, when calculating each new moving average, 1 level on the left is discarded and one level on the right is added.

For a quarterly series:

Let's consider the calculation of moving averages

| Period (year, quarter) | Initial levels (T/O) | Moving averages | Smoothed Centering Levels | Percentage |

| I quarter 2006 | 200,7 | 209,8 | 95,7 | |

| II quarter 2006 | 230,2 | 239,1 | 224,5 | 102,5 |

| III quarter 2006 | 198,4 | 250,9 | 245,0 | 81,0 |

| IV quarter 2006 | 327,2 | 250,1 | 250,5 | 130,6 |

| I quarter 2007 | 247,8 | 266,6 | 258,35 | 95,9 |

| II quarter 2007 | 227,1 | 256,6 | 261,6 | 86,8 |

| III quarter 2007 | 264,4 | 254,7 | 255,65 | 103,4 |

| IV quarter 2007 | 287,1 | 260,6 | 257,65 | 111,4 |

| I quarter 2008 | 240,2 | 266,9 | 263,75 | 91,1 |

| II quarter 2007 | 250,8 | 291,1 | 279,0 | 89,9 |

| III quarter 2008 | 289,5 | 308,0 | 299,55 | 96,6 |

| IV quarter 2008 | 383,7 | 336,6 | 322,3 | 119,1 |

Missing averages for the first quarter. 2006 and III, IV kV. 2008 are calculated by reducing the number of link levels

To smooth out the influence of random factors, we will center the moving averages by adding them in pairs and, in turn, finding their average.

We find percentage actual members of the original series to the corresponding moving average levels.

The seasonality index is determined:

Similarly we find

In this example, the moving average method is used to analyze the seasonality of trade turnover.

Similar analysis can be performed using simple average method. In this case, the following algorithm is used to calculate the seasonality index:

When calculating the seasonality index using moving averages, the general trend of increasing trade turnover from year to year is taken into account and therefore the calculated seasonality is more smoothed out - the first and third quarters are approximately the same. When calculating using the simple average method, the trend of growth in T/O from quarter to quarter is more pronounced, since the general trend of growth in T/O is superimposed on the quarterly seasonality.

Analytical alignment method. Consists in determining the approximating equation general trend changes in experimental values. For example, equations of a straight line or equations of a parabola, as was done earlier. The seasonality index is defined as the ratio of the actual values of the series members to their calculated value determined by the equation. The indices obtained in this way are averaged over quarters or months.

ANALYSIS OF THE FINANCIAL STATUS OF THE ENTERPRISE

Analysis of the financial condition of the enterprise is one of the main components economic analysis activities of the enterprise.

Depending on the purpose of the subjects of analysis, external or internal analysis of financial and statistical reporting is carried out. As a rule, the users and subjects of external analysis are creditors, investors, business counterparties (suppliers, buyers), tax services, etc. External analysis focuses mainly on open and public financial statements enterprises.

The purpose of internal analysis carried out by managers and owners of the enterprise is to assess the strengths and weaknesses financial and economic activities of the enterprise and determining the prospects for its development.

Main stages of analysis of financial and economic condition

1. Collection of information and processing of financial statements.

2. Analysis of the composition, structure of the enterprise’s property and sources of its formation.

3. Analysis of liquidity and solvency.

4. Analysis of financial independence, sustainability and stability of activities.

5. Analysis of indicators of business activity, profitability, price competitiveness, development strategy and tactics.

6. Analysis of the insolvency (bankruptcy) of the enterprise.

8. Development of measures to improve the financial and economic activities of the enterprise.

Stage 1. Collection of information and processing of financial statements

The basis for the analysis is financial and statistical reporting. Annual financial (accounting) statements of enterprises consist of 5 main forms:

1. Balance sheet (F1).

2. Profit and loss statement (F2).

3. Statement of changes in capital (F3).

4. Cash flow statement (F4).

5. Appendix to the balance sheet (F5).

The most informative form for analyzing and assessing financial condition is Form No. 1 (balance sheet). The balance contains a summary of information about the state household assets organizations included in Assets and the sources of their formation, components Passive. This information is presented at the beginning and end of the period (quarter, year), which makes it possible to compare indicators and identify trends in their change (growth or decline). In the Russian Federation, the balance sheet asset is built in order of increasing speed of transformation of these assets in the process of economic activity into monetary form, that is, in increasing order of the degree of liquidity of assets.

In the liabilities side of the balance sheet, the grouping of items is given on a legal basis, that is, all obligations of the enterprise are divided by subject: to the owners of the enterprise; to third parties (creditors). In turn, the external liabilities of the enterprise (borrowed capital, debts) are divided into long-term (for a period of more than 1 year) and short-term (for a period of up to 1 year). Liability items are grouped according to the degree of urgency of their repayment in ascending order. In first place is “Authorized Capital” as the most constant part of the balance sheet. The rest of the articles follow.

To illustrate the methodology for subsequent analysis of the financial condition, we present the analytical balance sheet of an enterprise. For simplicity, a number of non-core balance sheet items are not shown.

| Assets | Thousand rub. | Passive | Thousand rub. |

| I. Non-current assets, including: Intangible assets Fixed assets | III. Capital and reserves, including Authorized capital Retained earnings | ||

| II. Current assets, including Inventories Accounts receivable, including Long-term debt Short-term Short-term financial investments Cash Other current assets | - - | IV. Long-term liabilities, including loans and credits | |

| V. Short-term liabilities, including loans and credits Accounts payable Other short-term liabilities | |||

| Total Asset: | Total Passive |

Stage 2. Analysis of the composition, structure of property and sources of its formation. At this stage, the change in the value of the property as a whole, that is, the balance sheet asset, the change in the ratio between non-current and current assets, as well as the change in their total value are analyzed. Similarly, the change in the liabilities of the balance sheet, that is, equity and debt capital, as well as the relationship between them, is studied.

Stage 3. Analysis of the liquidity and solvency of the enterprise.

Liquidity of an enterprise is its ability to timely fulfill its short-term obligations. The main indicators characterizing liquidity and solvency are liquidity ratios and solvency ratio.

DS – cash;

KFV – short-term financial investments;

KP – short-term obligations (liabilities).

The absolute liquidity ratio shows what share of its short-term liabilities the company is able to pay off at the expense of the most liquid part of its assets. There is no standard value for this indicator. One of the recommended values is 0.05-0.2. High values of this ratio are beneficial for creditors, who, in the event of bankruptcy of an enterprise, will more easily receive their debts in the form of cash. From the standpoint of an operating enterprise, maintaining high values of this indicator is not at all necessary. During normal operation of the enterprise, the share of free cash flows may be very low. For example, in Japan the value of this coefficient is 0.01-0.02.

Liquidity ratios

SOS CO

SOS - own working capital (OA - KO);

SO - the most urgent liabilities (items from section V of the balance sheet).

On practice The solvency of an enterprise is expressed through the liquidity of its balance sheet. The main purpose of assessing balance sheet liquidity is to establish the amount of coverage of the enterprise's liabilities with its assets, the period of transformation of which into cash (liquidity) corresponds to the maturity of the obligations (repayment period).

To carry out the analysis, assets and liabilities of the balance sheet are classified according to the following criteria:

· according to the degree of decreasing liquidity (asset);

· according to the degree of urgency of payment of obligations.

This grouping of balance sheet assets and liabilities is presented in the diagram.

To determine the liquidity of the balance sheet, asset and liability groups are compared with each other.

|

The absolute liquidity conditions are as follows:

A1 P1; A2 P2; A3 PZ; A4< П4

A prerequisite for absolute balance sheet liquidity is the fulfillment of the first three inequalities.

The fourth inequality is of a balancing nature. Its implementation indicates that the enterprise has its own working capital (capital and reserves - non-current assets).

Less liquid assets cannot replace more liquid funds, therefore, if any of the inequalities has a sign opposite to that fixed in the optimal option, then the balance sheet liquidity differs from absolute.

Comparing A1 with P1 and A1 + A2 with P2 allows us to establish current liquidity, which indicates its solvency in the near future. Comparing A3 with P3 expresses long-term liquidity, which is the basis for forecasting long-term solvency.

The assessment of absolute indicators of balance sheet liquidity is carried out using an analytical table.

The assets of an enterprise, depending on the speed of converting them into money, are divided into 4 groups:

A1 – the most liquid assets – the enterprise’s cash and short-term financial investments. A1 = p.250 + p.260.

A2 – quickly realizable assets – accounts receivable and other assets. A2 = p.230 + p.240 + p.270.

A3 – slowly selling assets – inventories, as well as items from section I of the balance sheet asset “Long-term financial investments”. A3 = p.210 + p.220+p.140.

A4 – hard-to-sell assets – the result of section I of the balance sheet asset, with the exception of the articles of this section included in the previous group. A4 = p.190 – p.140.

Balance sheet liabilities are grouped according to the degree of urgency of their payment:

P1 - the most urgent obligations - accounts payable, other liabilities, as well as loans not repaid on time. P1 = p.620.

P2 – short-term liabilities – short-term loans and borrowed funds. P2 = p.610 + p.660.

P3 – long-term liabilities – long-term loans and borrowed funds. P3 = p.590.

P4 – permanent liabilities – equity capital that is constantly at the disposal of the enterprise. P4 = p.490 + p.630 + p.640 + p.650.

Liquidity ratios help determine a company's ability to pay its short-term obligations during the reporting period. The most important among them for financial management are the following:

· total (current) liquidity ratio;

· quick liquidity ratio;

· absolute liquidity ratio;

· net working capital.

Total liquidity ratio is calculated as the quotient of current assets divided by short-term liabilities and shows whether the enterprise has enough funds that can be used to pay off its short-term liabilities within a certain period. According to generally accepted international standards, it is believed that this coefficient should be in the range from one to two (sometimes three). The lower limit is due to the fact that working capital must be at least sufficient to pay off short-term obligations, otherwise the company will be at risk of bankruptcy. An excess of current assets over short-term liabilities by more than two (three) times is also considered undesirable, since it may indicate an irrational capital structure. When analyzing the coefficient, special attention is paid to its dynamics.

A partial indicator of the current liquidity ratio is quick ratio, revealing the ratio of the most liquid part of current assets (cash, short-term financial investments and receivables) to short-term liabilities. To calculate the quick liquidity ratio, another calculation formula can also be used, according to which the numerator is equal to the difference between working capital (excluding expenses in future periods) and inventories. In Russia, its optimal value is defined as 0.7 - 0.8.

In most cases, the most reliable is to assess liquidity only by the indicator of working capital. This indicator is called absolute liquidity ratio and is calculated as the quotient of cash divided by short-term liabilities. In Western practice, the absolute liquidity ratio is rarely calculated. In Russia, its optimal level is considered to be 0.2 - 0.25. and it is considered the most reliable coefficient.

Of great importance in analyzing the liquidity of an enterprise is the study net working capital, which is calculated as the difference between current assets and short-term liabilities. Net working capital is necessary to maintain the financial stability of the enterprise, since the excess of working capital over short-term liabilities means that the enterprise not only can pay off its short-term obligations, but also has the financial resources to expand its activities in the future. The presence of net working capital serves as a positive indicator for investors and creditors to invest in the company.

Change in liquidity level is established by the dynamics of the absolute value of net working capital. It is the amount of funds remaining after all short-term liabilities have been repaid. Therefore, the growth of this indicator reflects an increase in the level of liquidity of the enterprise.

Net working capital gives greater financial independence to the company in the event of a slowdown in the turnover of current assets (for example, with a delay in repayment of accounts receivable or difficulties in selling products), depreciation or loss of current assets (as a result of a fall in the value of finished products, bankruptcy of the debtor).

The optimal amount of net working capital depends on the characteristics of the company’s activities, in particular, on the size of the enterprise, sales volume, turnover rate of inventories and accounts receivable, conditions for providing loans to the company, on industry specifics and economic conditions.

The financial position of an enterprise is negatively affected by both a lack and a surplus of net working capital. The lack of these funds can lead the company to bankruptcy, since it indicates its inability to repay short-term obligations in a timely manner. The deficiency may be caused by losses in business activities, an increase in bad accounts receivable, the acquisition of expensive fixed assets without prior accumulation of funds for these purposes, the payment of dividends in the absence of corresponding profits, and financial unpreparedness to repay the enterprise's long-term obligations.

A significant excess of net working capital over the optimal need for it indicates inefficient use of resources.

| Liquidity ratio | Meaning | Calculation | Recomm. meaning |

| 1. General (current) liquidity | Adequacy of the company's working capital to cover its short-term obligations. It also characterizes the margin of financial strength due to the excess of current assets over short-term liabilities | working capital / short-term liabilities ((line 260 b. + line 250 b. + line 241 b. + line 210 b.) / total of section V b.) | 1-2 |

| 2. Urgent (intermediate liquidity, coverage ratio) liquidity | Predicted payment capabilities of the enterprise in the conditions of timely settlements with debtors | (Cash + Short-term financial investments + Net accounts receivable)/Short-term liabilities ((line 260 b. + line 250 b. + line 241 b.) / total of section V b.) | 0,7 -0,8 |

| 3. Absolute (fast) liquidity | What part of the short-term debt can the company repay in the near future (as of the balance sheet date) | Cash + short-term financial investments / Short-term liabilities ((line 260 b. + 250 b.) / total of section V b.) | ≥ 0,2 |

| 5. Own solvency ratio (SRR) | Characterizes the share of net working capital in short-term liabilities, i.e. the ability of an enterprise to repay its short-term debt obligations from net current assets | Net working capital/working capital | individual |

Since these parameters are momentary (shown in the balance sheet at the end of the quarter), it is advisable to calculate them over a number of periods. As a result, it is possible to build time series of solvency and liquidity indicators and give them a more objective and accurate assessment.

Balance sheet liquidity analysis

|

Name of asset group, calculation procedure |

Value, thousand rubles |

Name of the liability group, calculation procedure |

Value, thousand rubles |

Amount of payment surplus (deficiency), thousand rubles. |

|||||||||

During two periods, the enterprise has only one condition that does not meet the required ratio, namely, the most liquid assets do not cover the most urgent liabilities. The remaining conditions are met, therefore, the company can pay off long-term liabilities on time, and the excess of equity capital over non-current assets indicates that the company has its own working capital.

Let's calculate liquidity ratios (Table 6).

The absolute liquidity ratio decreased in 2013 by 0.01 and does not meet the standard values. Its value indicates that the company can pay off 10% of its short-term liabilities. The decrease in this indicator was due to an increase in accounts payable.

Table 6

Liquidity ratios of the organization

|

Indicator name |

Calculation procedure |

Normative value |

Actual value |

Change |

|||

|

Absolute liquidity ratio |

|

||||||

|

Intermediate liquidity ratio |

|

||||||

|

Current ratio |

|

||||||

|

Solvency ratio for the period |

|

||||||